Trump's Economic Approval Rating Drops To New Low As Market Sinks

By Andrew Mangan

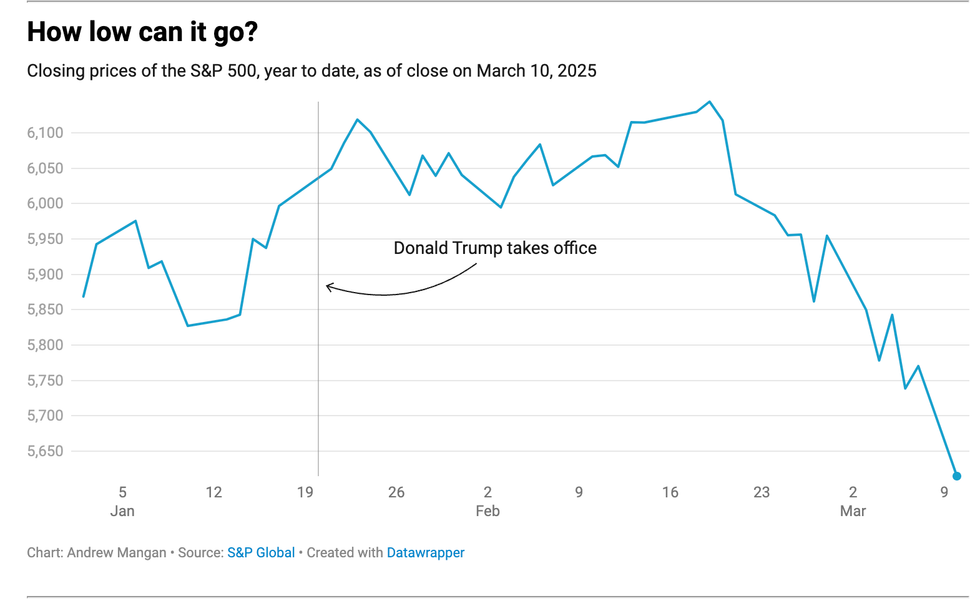

President Donald Trump is giving it his all—if by “it” we mean “wrecking the stock market and/or economy.” Despite a rally on Friday, the S&P 500 has tumbled 410 points and the Dow Jones Industrial Average has plummeted 2,537 points since Trump took office. And that pain springs from his nonsensical, reactionary tariff policy, which he is both backing off of and doubling down on at random.

And Americans are not happy.

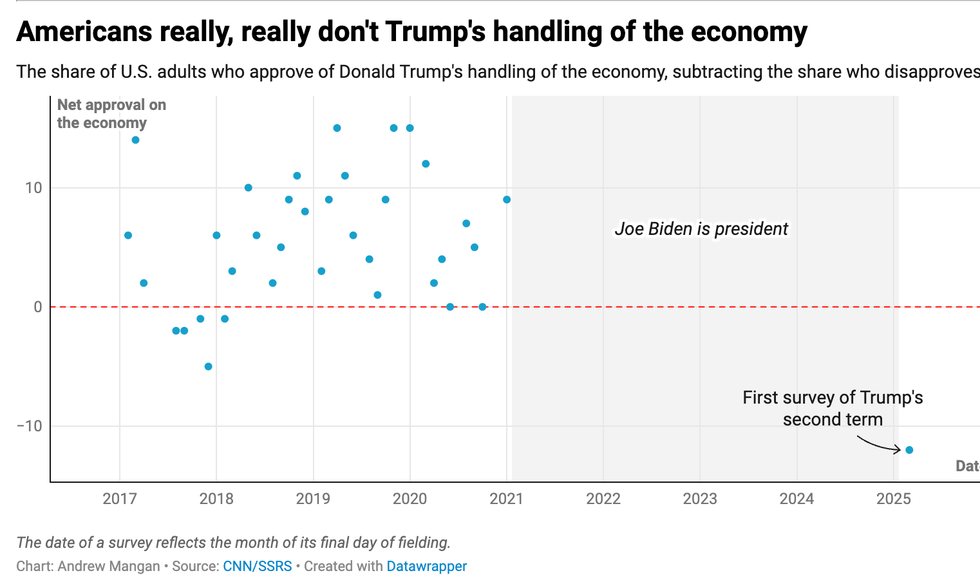

A new poll from SSRS conducted for CNN finds Trump with his lowest net approval rating on the economy ever. Just 44 percent of Americans approve of how he’s handling the economy, while 56 percent disapprove. That puts him 12 percentage points underwater.

His worst result before this in the same poll? Five points underwater, in December 2017.

Worse for Trump, this survey was finished fielding on March 9, meaning it was conducted before this past week’s stock sell-off. And Americans are largely aware of that market chaos: 41 percent correctly say stock prices have generally fallen since Trump took office, according to a YouGov poll fielded on Tuesday, amid the sell-off. Another 22 percent say they're about the same (wrong), while 15 percent say they're higher (wrong-er). But many of those folks might’ve had their minds changed since last Tuesday.

Naturally, Trump and his lackeys are blaming former President Joe Biden for the mess they created. And it is true that only 44 percent of Americans think Trump is more responsible than Biden for the state of the economy, while 34 percent blame Biden, according to a fresh YouGov poll for The Economist. However, that number will get worse for Trump the longer he is in office and pursuing this destructive trade war.

After all, nearly one-half of registered voters (46 percent) think Trump’s economic policies are hurting the economy, according to a new Emerson College poll largely fielded before the stock sell-off. That includes 81 percent of Democrats, 44 percent of independents, and 15 percent of Republicans. A mere 28 percent of voters think his policies are making the economy better, including just 55 percent of Republicans.

Another bad number for Trump? About one in four Republicans in Emerson’s poll think his tariff policies will hurt the U.S. economy, a view also held by four in five Democrats and more than one in two independents.

Given that Democrats’ and Republicans’ feelings about the economy tend to swing abruptly depending on who’s in the White House, those are pretty weak showings for Trump.

That said, while the Dow may be down 2,537 points, you can’t blame Trump. He’s been golfing a lot lately. He must think a negative number is a good one.

Reprinted with permission from Daily Kos